You can sell a house with an open insurance claim in Florida. However, as the seller, you need to clearly address a few key issues prior to the sale process, including:

- Disclosing known property damage

- Clarifying who will receive future insurance claim proceeds

- Deciding whether repairs will be completed before closing

- Determining whether to sell the property as-is or after repairs

The best path forward usually depends on the status of the insurance claim, the extent of the damage, and how quickly you want to sell.

This situation is especially common across Florida after hurricanes, flooding, roof leaks, water intrusion, and other storm-related property damage. Some homeowners choose to wait until repairs are completed before listing the property, while others decide selling “as-is” is the simpler option when repairs become too expensive, stressful, or time-consuming to manage.

The important thing to understand is that selling a house with an open insurance claim is about how the transaction is structured. Buyers, lenders, insurance carriers, and sellers all need clarity around the property’s condition, repair responsibilities, and insurance claim rights before closing.

If you are dealing with a damaged property anywhere in Florida, we buy houses as-is, including homes with pending insurance claims, storm damage, flooding, and major repair issues.

How to Sell a House with an Open Insurance Claim in Florida

Selling a house with an open insurance claim in Florida is possible, but the process requires more coordination than a standard home sale. Before listing the property or accepting an offer, it’s important to understand where the insurance claim stands, how the damage is being valued, whether additional insurance payments may still be available, and how those factors could affect the sale.

1. Review the Status of the Insurance Claim

Start by confirming exactly where your claim stands with the insurance company.

For example:

- Is the claim still pending or under investigation?

- Has the claim been partially approved or partially denied?

- Have any insurance payments already been issued?

- Are additional payments still tied to completed repairs?

These details can significantly affect both the sale process and the seller’s financial outcome.

You should also gather any documents related to the claim, including:

- The claim number

- Inspection reports

- Photos of the property damage

- Contractor estimates

- The insurance carrier’s repair estimate

- Any payment information already received

- Correspondence with the insurance company, public adjuster, or contractor

Make sure you also understand how the insurance carrier is valuing the damage.

Some claims are paid based on actual cash value (ACV), which factors in depreciation and usually results in a lower upfront payout. Others may include replacement cost value (RCV), where the insurance company may initially pay ACV first and then release the remaining recoverable depreciation after repairs are completed and documented.

That distinction can significantly affect your financial decision-making. If you sell the house as-is before repairs are completed, you may give up access to some or all recoverable depreciation tied to the claim. In situations involving major hurricane, roof, or water damage claims, the difference between ACV and full RCV payments can be significant enough to affect whether repairing the property before selling makes better financial sense.

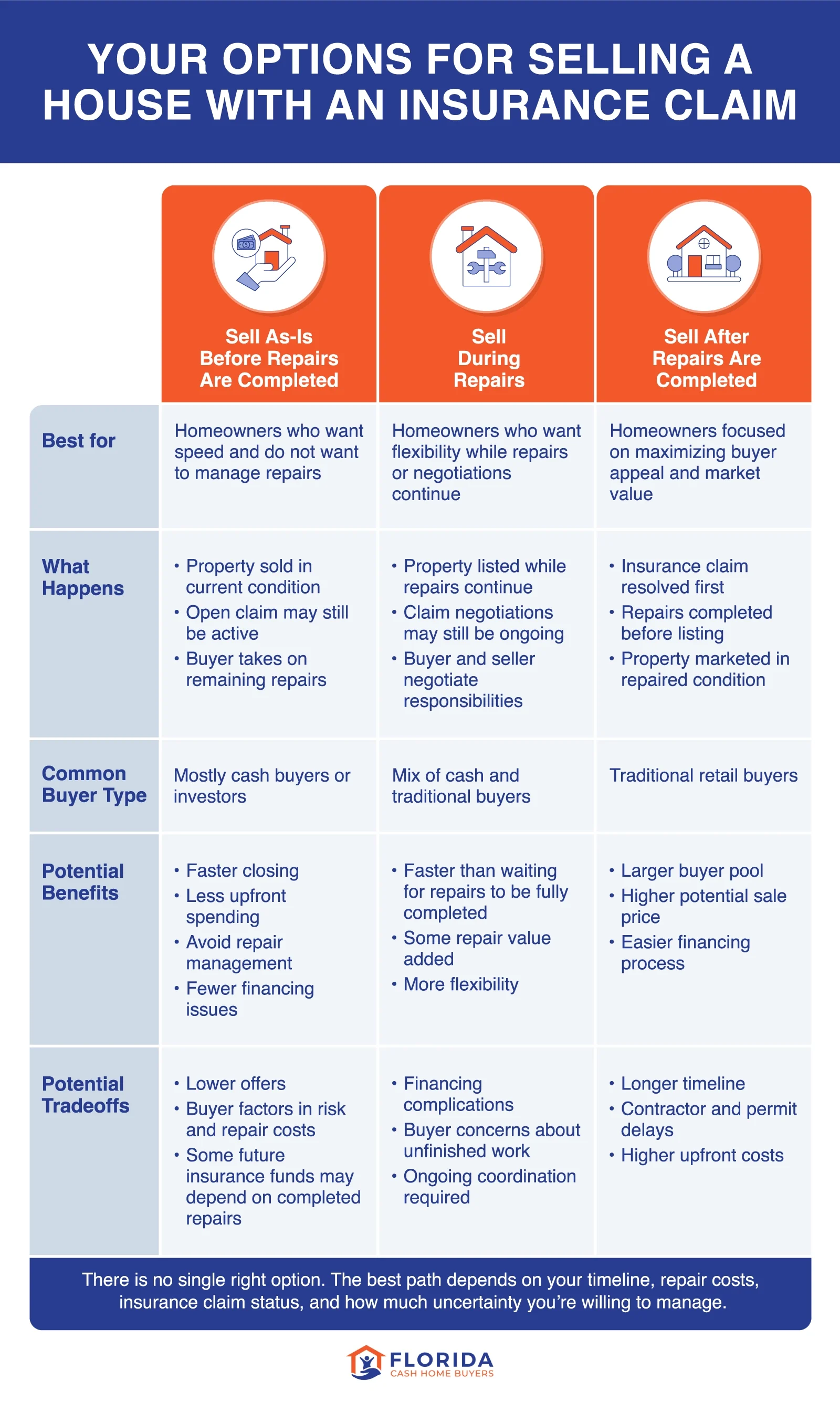

2. Decide How You Want to Sell

After you understand the status of the insurance claim and the condition of the property, the next step is deciding how you want to approach the sale.

The best option usually depends on:

- The severity of the damage

- How quickly you need to sell

- Whether repairs are cosmetic or structural

- How much insurance money is still tied to completed repairs

- Whether you want to manage repairs before closing

| Option | What This Looks Like | Best for | Potential Drawbacks |

|---|---|---|---|

| Sell the property as-is before repairs are completed | The home is sold in its current condition while damage, repairs, or insurance issues are still unresolved. This often involves cash buyers because traditional financing can become more difficult on damaged properties. | Homeowners who want to avoid repairs, contractor delays, financing issues, or ongoing insurance disputes | Cash buyers may offer less to account for repairs, risk, and unresolved damage. |

| Wait for the claim and repairs to be completed before selling | The insurance company resolves the claim, repairs are finished, and the home is listed afterward in fully repaired condition. | Sellers who are not in a rush and want a more traditional sale process | Repairs, permits, and claim delays can significantly extend the timeline. |

| Sell the home while repairs or claim negotiations are still ongoing | The property is listed while repairs, insurance negotiations, supplemental claims, or contractor work are still in progress. | Sellers who want to move faster without waiting for every repair item to be finalized | Buyers and lenders may still have concerns about unfinished work or unresolved claim issues. |

In general, waiting may make sense if repairs are manageable and remaining insurance proceeds are substantial. Selling as-is may make more sense if the claim is delayed, repairs are expensive, contractors are backed up, or you need a faster path forward.

Selling as-is is often the simpler option when:

- Repairs costs are large relative to your equity.

- The claim process is delayed or disputed.

- You cannot afford upfront repair costs.

- Contractors are backed up after a storm.

- The property has water, roof, flood, or foundation damage.

- You want to sell quickly instead of managing repairs.

If you’re unsure which path makes the most sense, Florida Cash Home Buyers can provide a free consultation to help you evaluate your options and determine whether selling the property as-is may be the simpler solution.

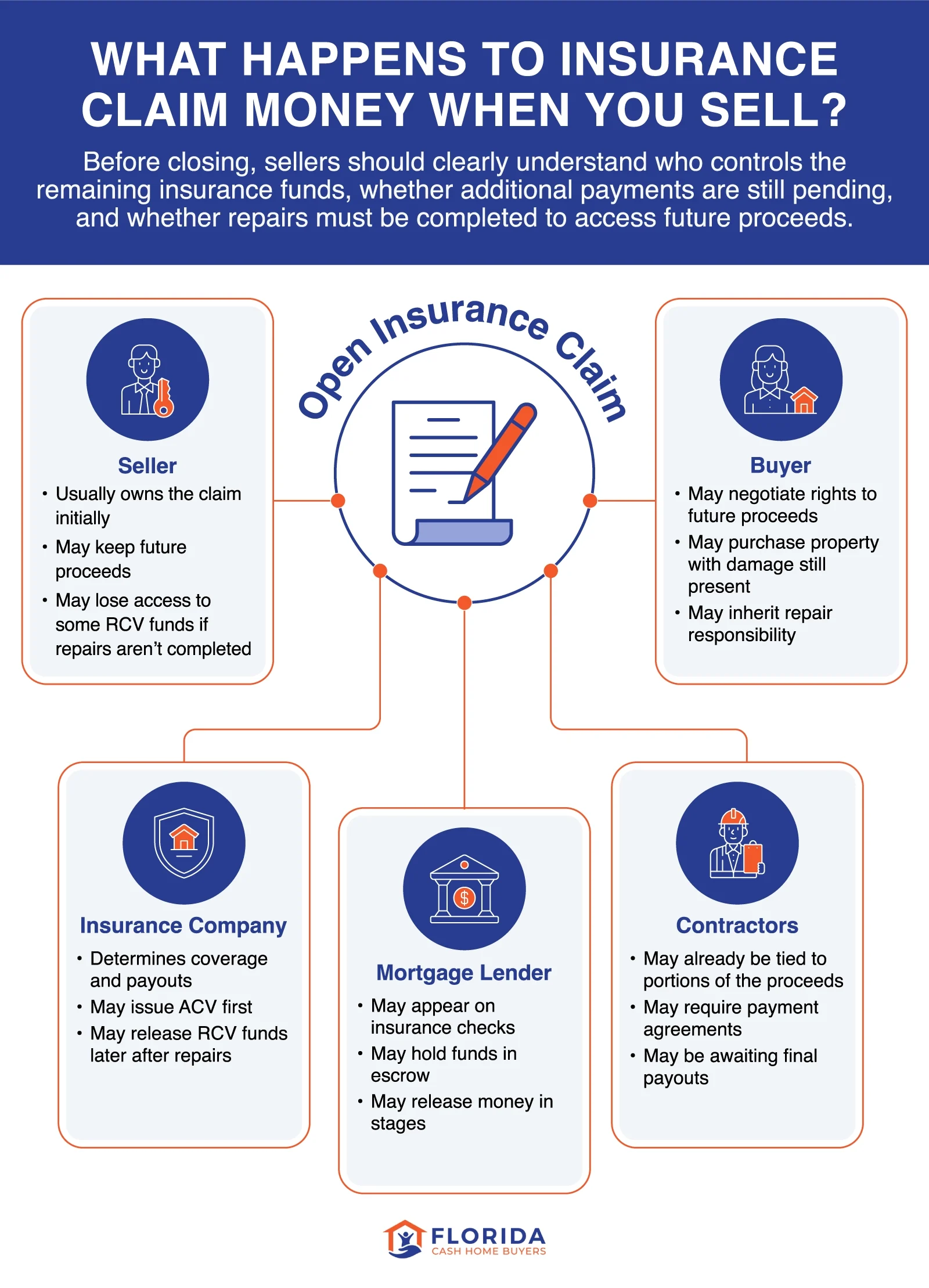

3. Clarify Who Controls the Insurance Claim Proceeds

Before the property goes under contract, it’s important to understand who controls any remaining insurance claim proceeds and whether all funds are actually accessible to the seller.

In many cases, the seller keeps the claim because they were the insurance policy holder when the damage occurred. However, that doesn’t always mean the seller has full control over the insurance funds during the repair process.

For example:

- Mortgage lenders are often named on insurance checks for major property damage claims.

- Some lenders may hold insurance proceeds in escrow and release funds as repairs are completed.

- Contractors or restoration companies may already have agreements tied to portions of the claim proceeds.

- Some replacement cost value (RCV) funds may not be released until repairs are completed and documented.

Because of that, sellers should fully understand:

- How much insurance money has already been paid

- Whether additional payments are still pending

- Whether recoverable depreciation is still available

- Whether the lender controls any portion of the funds

- Whether contractors, public adjusters, or service providers have payment agreements tied to the claim

Florida also changed its assignment-of-benefits (AOB) rules in January 2023. Under current Florida law, contractors generally cannot receive post-loss insurance benefits through traditional assignment agreements the same way they could previously. However, contractors, mitigation companies, or restoration providers may still have separate payment agreements or financial interests connected to the claim proceeds.

The purchase agreement should clearly address whether:

- The seller keeps future insurance claim proceeds

- Any insurance payments will be credited at closing

- Repairs are still pending

- Unrepaired damage remains at the property

- Any third parties have financial interests tied to the claim proceeds

Because insurance proceeds, lender requirements, and contractor agreements can directly affect the seller’s financial outcome, many homeowners choose to seek legal advice from a Florida real estate attorney or insurance professional before closing.

4. Disclose the Damage and Claim History

Under Florida law, sellers are generally expected to disclose known material defects that could affect the property’s value and may not be easily visible to the buyer. An open homeowners insurance claim often involves exactly those types of issues, especially when the property has unresolved or unrepaired damage.

This is especially important in Florida, where insurability has become a major issue in many real estate transactions. Significant storm damage, water intrusion, mold, roof problems, or unresolved claims can sometimes limit a buyer’s ability to obtain homeowners insurance, which may also affect mortgage approval.

Prior claims and unresolved damage may also appear in a property’s insurance history reports, such as a CLUE (Comprehensive Loss Underwriting Exchange) report, which some buyers and insurance carriers review when evaluating future coverage risk.

Depending on the situation, sellers may need to disclose:

- Hurricane or storm damage

- Roof leaks or roof damage

- Water intrusion or flood damage

- Mold

- Fire damage

- Structural or foundation issues

- Repairs already completed

- Repairs that are still pending

- Open or prior insurance claims tied to the property

Because of that, clear disclosure and documentation are extremely important when selling a house with an open insurance claim. Failing to disclose known issues can create legal and financial problems after closing, particularly if the buyer later discovers damage that was not disclosed during the sale.

That said, damaged properties still sell every day across Florida, especially to buyers who are comfortable purchasing homes as-is without traditional lender or insurance contingencies.

5. Price the Property Based on Its Current Condition

An open insurance claim can affect the sale price because buyers are not just evaluating the home’s market value. They are also considering repair costs, claim uncertainty, lender requirements, and the risk of hidden damage.

If you list the home traditionally, a realtor may recommend pricing the property lower to account for unresolved damage. Traditional buyers may also need lender approval, insurance coverage, inspections, and repairs completed before closing.

Cash buyers can often move faster because they are evaluating the home in its current condition. However, their offer will typically account for the home’s after-repair value, estimated repairs, holding costs, and the risk of taking on a damaged property.

6. Choose a Buyer Who Can Handle the Situation

Not every buyer is comfortable purchasing a home with an open insurance claim. Traditional buyers may need lender approval, insurance coverage, inspections, and repairs completed before closing. If the damage is significant, financing can become difficult.

Cash buyers are often more flexible because they can purchase the property as-is without lender-required repairs. This can be especially helpful if you want to avoid contractor delays, inspections, negotiations, or uncertainty around the claim process.

How an Open Insurance Claim Can Affect Selling Your House in Florida

An open insurance claim can affect nearly every part of the sale process, including buyer interest, financing, insurance coverage, negotiations, and final sale price.

The impact usually depends on:

- The type of property damage

- Whether repairs are cosmetic or structural

- The status of the insurance claim

- Whether insurance funds have already been paid

- The type of buyer purchasing the property

Buyer Concerns About Unresolved Damage

One of the biggest challenges with an open insurance claim is uncertainty.

For example, cosmetic damage like flooring, drywall, or minor roof repairs may feel manageable to some buyers. Structural damage, major water intrusion, mold, foundation movement, or unresolved storm damage often creates much greater concern because repair costs and long-term risks are harder to predict.

Potential buyers may worry about:

- Hidden damage that has not been fully uncovered yet

- Repairs becoming more expensive over time

- Mold or ongoing water intrusion

- Structural or foundation problems

- Delays with the insurance company

- Difficulty obtaining future homeowners insurance coverage

These concerns are especially common in Florida, where hurricanes, flooding, roof damage, and storm-related insurance claims are a regular part of the real estate market.

Why Financing Can Become More Difficult

Even if a buyer wants the property, the lender and insurance carrier may still create obstacles if the home has unresolved damage or pending repairs. Many lenders require homes to meet minimum condition and insurability standards before approving a mortgage.

That means financing can sometimes break down because:

- The property cannot secure acceptable homeowners insurance coverage.

- Repairs are considered too significant or safety-related.

- Appraisers flag unresolved damage.

- The lender requires repairs before closing.

- The insurance claim is still disputed or unresolved.

This is one reason many homeowners with heavily damaged properties eventually shift toward cash buyers, who can purchase homes as-is without lender-required repairs or financing contingencies.

How the Status of the Insurance Claim Can Change How You Sell

The status of the insurance claim itself can affect not only how the transaction works but also which selling approach makes the most financial and practical sense.

| Claim Status | What It Can Mean for the Seller | How It May Affect Your Selling Options |

|---|---|---|

| Claim approved with payments already issued | The sale may move more smoothly, but some replacement cost value (RCV) funds may still depend on completed repairs. | Waiting to complete repairs may help maximize remaining insurance payouts and market value. |

| Partial payout already issued | Additional recoverable depreciation may still be tied to repairs being completed and documented. | Selling as-is too early may reduce access to future claim funds. |

| Claim disputed or partially denied | Future payouts may be delayed or uncertain, which can affect repair decisions and negotiations. | Some homeowners decide selling as-is is simpler than continuing disputes or paying out of pocket for repairs. |

| Claim still under investigation | Repairs, claim decisions, and insurance payments may remain unresolved for months. | Sellers who need speed or certainty may prefer selling before the claim is finalized. |

As noted earlier, sellers with RCV policies should confirm whether any remaining funds depend on completed repairs before deciding to sell as-is. Under Florida Statute §627.7011, some insurers release additional replacement cost payments only after repairs are completed and documented. That doesn’t necessarily mean selling with an open insurance claim is a bad financial decision. For some Florida homeowners, the certainty and simplicity of selling as-is still outweigh the cost, delays, and uncertainty involved with continuing repairs and insurance negotiations.

How Cash Buyers Evaluate Homes with Insurance Claims

Homes with open insurance claims are usually priced differently than fully repaired properties because buyers are taking on additional risk, repair costs, and uncertainty.

What Cash Buyers Look at Before Making an Offer

When evaluating a damaged property, cash buyers typically look at both the condition of the home and the status of the insurance claim itself.

That evaluation often includes:

- The extent of the property damage

- Estimated repair costs

- Whether the damage could worsen over time

- Contractor and permit costs

- The status of the insurance claim

- Whether repairs have already started

- The possibility of hidden damage

For example, unresolved water intrusion, mold, structural movement, or storm damage may create more uncertainty because repair costs can continue increasing over time. Many buyers also evaluate the home based on its after repair value (ARV), which is the estimated market value once repairs are completed.

From there, they typically work backward by factoring in expected repair costs, holding costs, risk, and the complexity of the insurance situation.

Why Open Insurance Claims Can Lower Offers

Cash buyers usually factor additional risk into their offers when a property has unresolved damage or an open insurance claim.

That is because the buyer may be taking on:

- Repair expenses

- Holding costs

- Insurance uncertainty

- Market risk

- The time required to complete repairs

The more uncertainty surrounding the property or claim, the more conservatively buyers tend to evaluate the deal. However, that does not always mean selling as-is leaves the homeowner worse off financially.

Cash buyers also evaluate the costs sellers may avoid by not completing repairs themselves, including:

- Additional out-of-pocket repair costs

- Realtor commissions

- Taxes, utilities, and insurance payments while the property sits

- Financing fallout from traditional buyers

- Ongoing delays tied to contractors or insurance negotiations

Because of that, many Florida homeowners decide the speed, certainty, and simplicity of an as-is cash sale outweigh the potential upside of waiting for repairs to be completed.

If you want to avoid repairs and ongoing insurance headaches, Florida Cash Home Buyers purchases houses throughout Florida as-is, including homes with pending insurance claims, storm damage, flooding, and major repair issues.

A Simpler Way to Sell a House with an Insurance Claim in Florida

Selling a house with an open insurance claim in Florida is possible, but the process can quickly become stressful when repairs, insurance delays, contractors, and financing issues all start overlapping.

For homeowners who don’t want to keep managing the damage and claim process, Florida Cash Home Buyers offers a simpler way to sell. We buy houses throughout Florida as-is, including properties with pending insurance claims and major repair problems.

That means:

- No repairs or cleaning

- No realtor commissions

- No lender-required repairs

- Fast and flexible closing timelines

- Help navigating difficult selling situations

Instead of waiting months for repairs or insurance disputes to be resolved, homeowners can sell the property in its current condition and move forward with more certainty and less stress.